Why is it called Apple Watch

Apple announced a revolutionary product in Apple Watch. The name does not strike a cord for many. The dissatisfaction is palpable and understandable given the promise of a computer on wrist and the possibilities that enables. It will be much more than a watch. But why call it Apple Watch?

As Horace Dediu succinctly put

Apple product names are usually intuitive and convey the intended use directly. Just to pick a few: Numbers, Mail, iPhoto, Apple TV, Thunderbolt, Lightning – All these names make sense and convey the intended use directly. In light of this the name Apple Watch seems to be a disservice for the potential it shows.

However promising the prospects of iPhone might have been in 2007 it is hard for anyone to predict what would become of the iPhone a few years later. The killer apps for iPhone did not exist in 2007. Same goes for the Apple Watch in 2014.

What do you name a product when you do not clearly know what it would evolve into if you are used to naming products to convey exactly what they are meant for?

The safe bet is to name the product to convey the one essential function that is well defined, it will always do, and can be called upon to do anytime. For iPhone the essential/bare-minimum function guaranteed to always work is making phone calls. For Apple Watch it is telling time.

Horace Dediu reminds us of the Tentpoles around which iPhone and Apple Watch were launched

When the iPhone launched, Steve Jobs introduced it as being three products in one:

– A wide-screen iPod

– A phone

– A breakthrough internet communicatorWhen the Apple Watch launched, Tim Cook introduced it as being three things:

– A precise timepiece

– A new, intimate way to communicate

– A comprehensive health and fitness device.

Of the three tentpoles for iPhone only the phone part is a novelty in an apple product and well defined – Phone part of iPhone works the same way since day one. Although it would be a disservice to the product, an iPhone can be used just as a phone. iPod functionality existed in the iPod. Internet communicator functionality was not well defined – at least not the way it would power novel applications a few years down the line. It seems natural that Apple would name this product Phone.

Of the three tentpoles for Apple Watch only the timepiece part is well defined and guaranteed to work the same way from day one. Timepiece functionality is a novelty in an Apple product. Timepiece functionality will not improve significantly – Accuracy within 15 msec is way more than good enough. The other two tentpoles do not pass this test: intimate communication device and health/fitness device parts are far from well defined and will see significant improvements in future version. It seems natural that Apple would name this product Watch.

Now does it make sense to call them iPhone, Apple Watch?

Instacart, Soylent, hobbies

Every week I go on a trip to the local grocery stores to stock up the kitchen and the fridge. Most of the time I have to go to multiple stores – this is partly because some of what I want is available only in a particular store; and partly from observations on quality, pricing differences on items that are available at multiple stores. I understand this behavior is common. Most people do this weekly ritual on weekends. Stores plan for the rush on weekends and are often not as well stocked on the lean days. While the economy is attuned to this man-made construct called work-week and weekends, mother nature treats all days equally. Vegetables, flowers and fruits do not plan backwards from weekends and account for transportation and harvesting.

I have often wondered what a waste of time these weekly grocery trips are, more so if the day thus far had not been very productive. I am sure many have felt this way and wondered if there was a way out.

People pay for convenience. The folks at Instacart, and investors like Andresseen-Horowitz are betting that enough people will pay for this convenience.

Several questions arise:

- Does the typical shopper buy groceries from one store?

- Given that Instacart charges by the store “For most stores, delivery in under 2 hours is just $3.99” Will someone hire Instacart for several stores?

- Will someone hire Instacart several times a week for the same store to get fresher produce?

Routines and rituals punctuate our lives. I enjoy the time when the whole family goes on these grocery trips. Such trips are clearly marked during the week. May be I am in the minority.

I see the benefit of services like Instacart in saving time and effort for many people. Even to this day households in many parts of the world buy vegetables and fruits from hawkers. May the developed world is going back to the convenience of getting produce right from home; services like Instacart provide an added convenience of choosing from a much bigger selection than the vendor can transport on a cart.

That brings me to the next topic doing rounds in my head in recent days: Soylent.

Food is integral to culture – at least so far. We make plans for social gatherings around food. Ceremonies are commemorated with elaborate feasts. Countless conversations end with “How about we meet for lunch sometime next week.?” It reminds me of the famous The New Yorker cartoon. “How about never — Is never good for you?”

People point out that food cannot be replaced by a concoction like Soylent and that it is doomed to fail. Not every meal is conversational, socializing, etc., Just ask how many meals are eaten alone at the desk. Chris Dixon put it succintly.

According to Soylent critics, every non-Soylent meal is a joyous family gathering featuring organic food and edifying conversation.

— Chris Dixon (@cdixon) May 19, 2014

The mistake in this analysis of Soylent haters is that Soylent will replace food completely. As Balaji Srinivasan pointed out, Soylent will not be a substitue for all food in the near future or may be never. Soylent can substitute snicker bars or milk shakes that go between meals. It is highly unlikely Soylent will replace entire meals for anyone outside the die-hard fans. Soylent will definitely not replace grilling with friends at the local park or the family dinner or the dinner at a friend’s house. It does not have to. The job that Soylent addresses is satisfying hunger quickly, possibly lonely meals.

The thing people don’t get about @soylent is that it’s a replacement for Snickers bars, not salad. A better default than junk food.

— Balaji S. Srinivasan (@balajis) May 5, 2014

I am not convinced that food can be replaced by a concoction of checmical ingredients. The reason is that we can only test and create synthetically what we know about food.

Societies evolve. Daily affairs of lore are now hobbies. Eg: hunting, running, grilling, gardening, camping. Will trips to the grocery stores and cooking for oneself go this way? I am not convinced.8

Workspaces On Tablets

Tablet computers are shared much more than desktop or laptop computers. However, there is no privacy or individual workspace on a tablet. Tablets have lacked the individual logins available in desktop and laptop computers.

I understand there are resource constraints on Tablets. I am eager to see the day when TouchID will be used to recognize the user and show the applications associated with the user. Even if this provision is not full scale, it would immensely help parents who share a Tablet with children to limit what the children can access.

Apps are silos. We can limit the silos available to individual users.

Ignorance and Expertise

There are simply too many things going on for any one person even to know the key basics in every relevant field, never mind become an expert or have some insight.

…

No-one can be an expert on all of those

Benedict Evans on Limits of Knowledge

I completely agree with Benedict. When one person can not synthesize a multitude of areas, a team of experts is the answer. Each person in this fictional team is a “T” expert — meaning having a decent understanding of a variety of areas and a deep understanding in the area(s) of core concentration. When the understanding of such a team is put together the result is a solid understanding. One needs to be careful to have few gaps between the stems of “T”s to avoid cracks and blind spots.

ebook-bundling

Almost three years ago I wrote on how asking to pay for a physical book and e-book separately was double charging. Amazon announced Kindle MatchBook. It is still not giving e-book for free with a physical book. It is close enough.

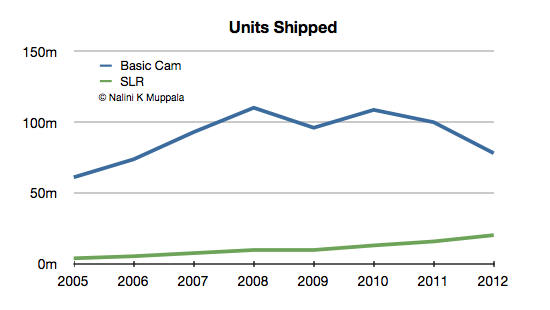

Digital Camera Trend In 2012

Here is an update on digital camera market performance in 2012. The Camera and Image Products Association of Japan provides data on the number of units produced, shipped and their value. Most major digital camera vendors participate in this research. With a majority of digital camera vendors hailing from Japan, the data from CIPA is a good proxy for the industry. Let us read into the trend based on the shipment data.

- SLR camera unit shipments continued to grow. 2012 saw 28% more shipments.

- One in 5 digital cameras shipped was an SLR.

- Basic camera shipments continued to decrease. 2012 saw 22% fewer shipments. This is the worst drop since 2006.

- 2012 saw a break in price erosion of the past several years. Basic cameras held the price. SLRs on the other hand reversed the trend and sold for higher price.

- Price of basic camera, on average, held steady at $115.

- SLR camera ASP went from $429 to $467.

- On the whole ASP improved significantly to $187.

- SLRs accounted for 51% of total revenue.

- Revenue from basic cameras fell by 22%.

- SLR revenue increased by 41%.

- Overall revenue increased slightly.

All the above charts are based on US Dollar equivalents (1 JPY = 0.0125 USD) of prices and revenues reported in Japanese Yen.

The following table shows growth rates of various aspects.

Square

Square payments is a disruptive innovation. Square started as a new market disruption by enabling people who until then could not accept credit/debit card payments, to do so from the convenience of a smartphone or an iPad. As expected, according to theory of disruptive innovation, there was no response from the incumbents.

Again in line with disruptive innovation theory, as incumbents are expected to, Square moved up market with its Register app that turns an iPad into a register. Register is also a low cost disruption. It is much cheaper to get started with a Square App on a iOS device than to install a traditional “cash” register. Incumbents will start feeling the pressure now.

A primary advantage that Square has over traditional can registers is that it is a software solution. Product enhancements are cheap and easy for the merchant. It rides on the mobile device boom. Imagine the possibilities for the passenger in a Taxi cab fitted with a iPad for Square Register, news updates: news updates, email, … endless.

I think Square activity will be a barometer of the economy. It will be a window into consumer behavior similar to FedEx shipment trends, payroll churn data from ADP. Such insight in its raw form might not be of commercial value to Square. Remember Mint? Mint provided a convenient way to gather credit cards, loans, banking accounts, and stock trading accounts in one place to get a complete picture of one’s finances. Mint was able to gather some insight into consumer behavior. However, Mint failed to create a thriving business model to leverage such insight, and was acquired by Intuit. Mint.com continues to pitch credit card, loan offers that could lead to savings. the pitches are customized based on user activity (annual fee on a credit card, APR, etc.,). However the revenue from providing customer leads was clearly not big. As @asymco says, Square is sitting on a mountain of valuable data. I suspect they will find a way to leverage it and thrill users with better experiences, even if not monetize it directly. Yes, the age of Big Data.

There has been much talk about NFC for payments. NFC requires more change in user habits than the solution pioneered by Square. With Square, people continue to use their credit cards and pay their bills at the end of the month as they always did. Merchants need not retool to accept NFC payments; Square builds on the millions of mobile devices in merchants’ and consumers’ hands. But this leads us to what is missing in Square.

An element of disruption is missing in the way Square works now. Square accepts traditional credit cards and debit cards as the only mode of payment. The value chain still includes payment clearance houses which presumably take a cut of the 2.75% processing fee that Square charges for every transaction.

I suspect Square is working on a means to eliminate payment processing houses from the value chain. Preloading user account with money is the quickest; direct debit from a bank account might be easy; mimicking credit card functionality is the toughest: there is a lot of risk in providing credit to user and ask to be paid later. Given the prevalence of credit card usage, Square would have to live with payment clearance houses until it cracks the hard one. No wonder then Visa is one of the early stage investors in Square. Linking a checking account to Square might be the best in the short term.

There will be copy cats and the first one is Paypal Here. Again, this includes payment clearance houses. For now, Paypal’s advantages seem minimal: a slightly smaller processing fee at 2.7% (vs Square’s 2.75%), same day availability of funds in merchant’s paypal account (vs Square’s next day to merchant’s checking account). Paypal is limited to Paypal users, Square is open to anyone using a smartphone and a credit card.

Competition is not standing still. The opportunity in mobile payments is big and everyone would love to have a piece of it. Just one example: Mobile network operators are hard at work via Isis. MNOs have been seeing less love these days though.

Square is promising.

Image source: NYT bits blog

Digital Camera Trend In 2011

Production and shipment data for digital cameras from Japanese vendors is now available for all of 2011. I had discussed the data from 2010 in an earlier post here. The Camera and Image Products Association (CIPA) of Japan provides data on the number of units produced, shipped and their value. Most major digital camera vendors participate in this research [pdf]. With a majority of digital camera vendors hailing from Japan, The data from CIPA is a good proxy for the industry. Let us read into the trend based on the shipment data.

- SLR camera shipments continued to grow. Shipments increased 22% in 2011.

- SLR camera growth was the lowest in six years apart from the across-the-board bad year in 2009.

- For the second time in six years, basic camera shipments decreased on an annual basis.

- SLR units accounted for 13.58% of total shipments.

- Prices of both SLR and basic cameras continued to fall. On average, a SLR camera sold for $429, and a basic camera went for $116.

- The price erosion was much less than previous years.

- On the whole, ASP in $ terms improved slightly to $158.

- SLRs accounted for 63% of total revenue in 2011.

- For the second time in six years, revenue from basic cameras fell.

- SLR revenue increased but failed to make up the decrease in basic cameras, resulting in a reduction in overall revenue for the year.

All the above charts are based on US Dollar equivalents (1USD = 79.70 JPY) of prices and revenues reported in Japanese Yen. Yen strengthened again in 2011, adding to Japanese vendors’ woes. In Yen terms, the performance was worse. The following table shows growth rates of various aspects.

You must be logged in to post a comment.